One way to look a the future is to check how China is doing to far since they were the first impacted and based on data coming from the government managed to contain SARS-CoV-2 virus by the end of February 2020.

|

| COVID-19 Cases in China |

The PMI dropped sharply in February to 35.70 points, but we still have to wait longer to know the extent of the rebound in March and April.

Many businesses have re-opened, and while Hubei province has recently re-opened its borders (March 28), neighboring provinces are still wary of letting people travel. We also have contact in China, that non-essential business (e.g. entertainment) will not re-open until the end of April, and that's in Liaoning far from the epicenter in Wuhan. So in China, it's quite possible the local economy returns to normal in May. It would have been 4 full months since the beginning of the spread of the disease. However, China's GDP will certainly be impacted by the drop of activity in the rest of the world that is around 1.5 months behind in terms of cases.

My best-case scenario where the virus is contained around the world as fast as it was in China is that activity returns to "normal", yet somewhat lower levels, in July 2020. That would mean a sharply higher quarter-on-quarter Q3 GDP (worldwide), but still fairly lower year-on-year.

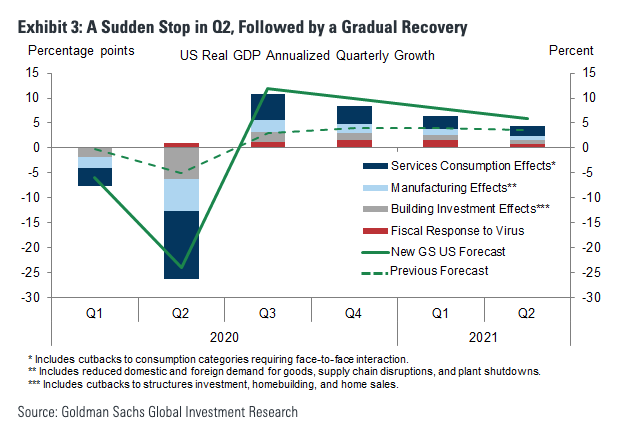

This assumes somehow few businesses and consumers bankruptcies, not currency crisis following helicopter money from central banks, or any other major financial issues related to the COVID-19 shutdown. How likely is that I'm not so sure, but this was the view of Goldman Sachs around a week ago with a 24% GDP drop in Q2 in the US, followed by +10% in Q3, and +8% in Q4 with the full year down 3.8%.

That would be a short recession, but considering how the US stock market was extended in February 2020 (and still is), problems are likely to linger much longer in the US, and many other countries.

Viruses are also interesting creatures, and earlier this month, we tried to look at the 1918-1919 Spanish flu to understand the economic and market impact of the novel Coronavirus, and we posted this chart representing the numbers of death per 100,000 in the UK at the time.

Viruses come in waves. It started in June-July 1918, then dropped until around early October, before coming back with a vengeance until the end of December with a small retrieve in January, before the last wave topping in in March 1919 before ending at the end of May 1919.

If this pattern occurred again that would be mean on and off lockdowns over a 10+ month period in each country, meaning nearly 12 months of lower economic activity worldwide, and the greatest depression we've ever seen. I have no clear idea what the world would look like in that case but there would be a low economic activity, out of control money printing, resulting in inflation down the road especially if they keep giving money directly to citizens also called MMT (Modern Monetary Theory) leading to the inflationary depression touted by Peter Schiff, at least in the US and the western world.

How will it exactly pan out? We just don't know, nor does anybody and only time will tell, but everybody should be aware of the risks and prepare at best as they can.