- 2013, The First Steps into The "World Afterwards" in Complete Chaos - As the world enters into a global recession in 2013, it will become more fragmented into regional blocks. Although the Euroland, South America and Asia should come strengthen from the crisis, the US, the United Kingdom, Israel and Japan should be greatly weakened.

- Politics in Germany until 2017 – Weaking of main political parties, and increase in the number of small parties.

- Yearly evaluation of LEAP anticipations – 75% success rate en 2012. By their own assessment, before new anticipations are published in GEAB 71 next month.

- Global systemic crisis: Assessments of 40 « country-risks» - LEAP 2020 team looks into 40 countries, and how they are likely to handle the 2013 crisis.

- Strategic and operational recommendations. Stock markets are likely to slide downwards, banks will suffer and it may be wise to spread assets among several banks, prudence is required when investing in real estate, and keep stocking up Gold.

- The GlobalEurometre - Results & Analyses. 66% (vs 48% in November) of respondents experienced price increases..

Showing posts with label inflation. Show all posts

Showing posts with label inflation. Show all posts

Saturday, December 15, 2012

GEAB 70 - 2013, The First Steps into The "World Afterwards" in Complete Chaos

Here are the highlights of GEAB 70 (December 2012) entitled

"2013, The First Steps into The "World Afterwards" in Complete Chaos":

Friday, June 1, 2012

Marc Faber June 2012 Market Commentary

Marc Faber has just released his June 2012 market commentary on the gloomboomdoom.com website.

This month report is entitled "The Political Function of Inflation is to Mislead Public Opinion" and he talks about the distortions created by inflation. He explains that scholars had longer discovered the viciousness of monetary inflation long time ago quoting Nicholas Oresme (14th century):

He carries on saying that we need to consider seriously Sheila Bair’s tongue-in-cheek proposal to fix income inequality with a $10 million loan for everyone, especially if we are to believe the Keynesians that the "economy desperately needs a short run fix" (Krugman).

The main issue is that Keynesian economic policies are directly responsible for the current global economic crisis, because they have led to excessive debts in most Western societies, which will remain for a long time and be a drag on growth.

There is only 1 attachments with this monthly market commentary (MMC):

If you want to access the full Monthly Market Commentary (MMC) by Marc Faber, it is available for 300 USD per year.

PS: Last month he also issued a temporary (and short) report in the middle of the month. I don't have access to it, but this kind of "urgent" report is usually not a good thing...

This month report is entitled "The Political Function of Inflation is to Mislead Public Opinion" and he talks about the distortions created by inflation. He explains that scholars had longer discovered the viciousness of monetary inflation long time ago quoting Nicholas Oresme (14th century):

Among the many disadvantages arising from alternation of the coinage which affects the whole community is....that the prince could thus draw to himself almost all the money of the community and unduly impoverish his subjects. And as some chronic sicknesses are more dangerous than others because they are less perceptible, so such an extraction is more dangerous the less obvious it is.

He carries on saying that we need to consider seriously Sheila Bair’s tongue-in-cheek proposal to fix income inequality with a $10 million loan for everyone, especially if we are to believe the Keynesians that the "economy desperately needs a short run fix" (Krugman).

The main issue is that Keynesian economic policies are directly responsible for the current global economic crisis, because they have led to excessive debts in most Western societies, which will remain for a long time and be a drag on growth.

There is only 1 attachments with this monthly market commentary (MMC):

- "Natural Gas: A Contender for the Greatest Thematic Tailwind over the Next 20 Years" by Pedro Noronha, Noster Capital LLP

If you want to access the full Monthly Market Commentary (MMC) by Marc Faber, it is available for 300 USD per year.

PS: Last month he also issued a temporary (and short) report in the middle of the month. I don't have access to it, but this kind of "urgent" report is usually not a good thing...

Tuesday, April 3, 2012

Marc Faber: Inflation or Deflation ?

Marc Faber is interviewed by Lauren Lyster's Capital Account on Russia Today on the 3rd of April 2012.

Marc Faber says inflation in money and credit can cause bubbles, but it is hard to know where they are, and it is not easy to know where inflation is taking place. He also notes that governments hide inflation and much of that inflation goes into asset prices. We do not know exactly how much the Federal Reserve, the ECB, the BOJ, etc. are propping up the prices of stocks, commodities, etc. We can only estimate. The money printing and loose language of the central bankers and policy makers around the world certainly does distort the price mechanism, however, and Marc Faber is not optimistic about the ramifications of these actions.

He also mentioned the quadrillions in derivative, and that derivatives bubble will eventually collapse and lead to massive wealth destruction.

When asked to give advice to young people in their 20s and 30s, he referred to his generation and how it was easy to get a job at the time, but since the collapse of communism and the advance of the internet, 3 billion persons entered the world economy and western youngster have a lot of competition by young people living in developing economies, so he just think young people should lower their expectations and people in the western world should change their mentality and reject the nanny state.

The interview starts at 3:18.

Marc Faber says inflation in money and credit can cause bubbles, but it is hard to know where they are, and it is not easy to know where inflation is taking place. He also notes that governments hide inflation and much of that inflation goes into asset prices. We do not know exactly how much the Federal Reserve, the ECB, the BOJ, etc. are propping up the prices of stocks, commodities, etc. We can only estimate. The money printing and loose language of the central bankers and policy makers around the world certainly does distort the price mechanism, however, and Marc Faber is not optimistic about the ramifications of these actions.

He also mentioned the quadrillions in derivative, and that derivatives bubble will eventually collapse and lead to massive wealth destruction.

When asked to give advice to young people in their 20s and 30s, he referred to his generation and how it was easy to get a job at the time, but since the collapse of communism and the advance of the internet, 3 billion persons entered the world economy and western youngster have a lot of competition by young people living in developing economies, so he just think young people should lower their expectations and people in the western world should change their mentality and reject the nanny state.

The interview starts at 3:18.

Monday, March 26, 2012

Peter Schiff: Ben Bernanke is Public Enemy No. 1

Peter Schiff is interviewed on CNBC Fast Money on the 26th of March 2012 and explains the Federal Reserve is now blowing a massive bubble in US treasury and government debt and once this pops (as interest rate must be increased due to inflation), banks will fail and the crisis will be worse than 2008/2009.

Saturday, March 17, 2012

The Next 20 Years: Inflation vs Deflation

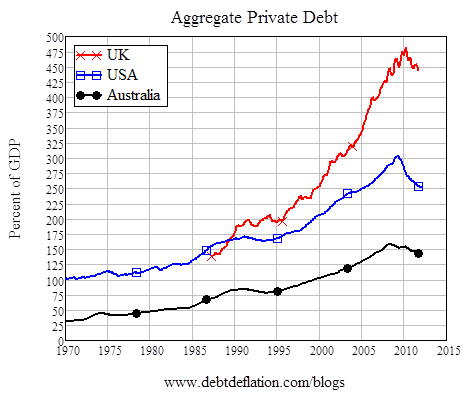

Steve Keen, an Australian economist and contrarian strongly opposed to neo-classic economists views, has recently posted an article entitled "Economics without a blind-spot on debt" where he discusses the importance of private debt during the great depression and now.

He managed to gather the data for aggregate private debt in the US and Australia and drew the result in the chart below:

There was a debt bubble in the 30s which led to the great depression, and now it appears we have the same kind of bubble, only more pronounced. The main difference is that now we live in a world of fiat currencies and what happens next is highly depending on monetary policies.

There was a debt bubble in the 30s which led to the great depression, and now it appears we have the same kind of bubble, only more pronounced. The main difference is that now we live in a world of fiat currencies and what happens next is highly depending on monetary policies.

I encourage you to read his blog post for details about private debt. I'm going to focus on 2 scenarios:

In this scenario, there would be massive deflation, and, in theory, the preferred asset would be cash (under the mattress) and many companies and banks would have to go bankrupt, but in reality, the system would probably have to collapse, and I'm not so sure what the value of cash would be. This is the kind of scenario envisioned by Robert Prechter who sees the Dow Jones at 1000 USD.

The other scenario (flat private debt to GDP ratio) would assume massive money printing. Let's assume somehow the federal reserve can keep this ratio constant by printing money during 23 years. If the GDP growth is flat, it would require about 3% (extra) inflation per year. However, during that period, there is actually a good chance of negative growth because Peak oil consequences will be in full effect unless we find some energy alternatives. This also excludes public debt and unfunded liabilities (about 100 trillions USD or 600% of GDP) which would require inflation north of 10% to get monetized.

If you think the US is in bad shape, just look at the aggregate private debt in the UK in the chart below. This country (and the British pound) are going to have a very rough time in the years and even decades ahead, as its private debt stands at 450% of GDP.

You may also want to read "Currency Crisis:Why is the British Pound a doomed currency ?" for a more detailed analysis of the United Kingdom debt and upcoming GBP currency crisis.

You may also want to read "Currency Crisis:Why is the British Pound a doomed currency ?" for a more detailed analysis of the United Kingdom debt and upcoming GBP currency crisis.

He managed to gather the data for aggregate private debt in the US and Australia and drew the result in the chart below:

I encourage you to read his blog post for details about private debt. I'm going to focus on 2 scenarios:

- Deflation where the central banks do not really fight the debt deflation (or debtflation).

- Inflation where the central banks decide to keep the aggregate private debt constant and works thru the years via inflation.

In this scenario, there would be massive deflation, and, in theory, the preferred asset would be cash (under the mattress) and many companies and banks would have to go bankrupt, but in reality, the system would probably have to collapse, and I'm not so sure what the value of cash would be. This is the kind of scenario envisioned by Robert Prechter who sees the Dow Jones at 1000 USD.

The other scenario (flat private debt to GDP ratio) would assume massive money printing. Let's assume somehow the federal reserve can keep this ratio constant by printing money during 23 years. If the GDP growth is flat, it would require about 3% (extra) inflation per year. However, during that period, there is actually a good chance of negative growth because Peak oil consequences will be in full effect unless we find some energy alternatives. This also excludes public debt and unfunded liabilities (about 100 trillions USD or 600% of GDP) which would require inflation north of 10% to get monetized.

If you think the US is in bad shape, just look at the aggregate private debt in the UK in the chart below. This country (and the British pound) are going to have a very rough time in the years and even decades ahead, as its private debt stands at 450% of GDP.

Wednesday, February 29, 2012

Marc Faber March 2012 Market Commentary

|

| Image by Getty Images via @daylife |

This month report is entitled "When we are no longer able to change a Situation, we must change ourselves", possibly referring to the massive debt load of western economies and the change of attitude required in those economies.

There is one attachment with this monthly market commentary (MMC):

- "China's Leadership Transition - Social Stability May Require a Stronger Renminbi" by Kieran Osborne, Director of Research of Merk Investments.

He concludes as follows:

Any marginal change in the governance of China is likely to have far reaching implications. Most notably, we expect an increased focus on developing the Chinese middle class and domestic economy over time, with less reliance on the export sector. In turn, political and economic realities are likely to force Chinese policy makers to allow the RMB to appreciate, to help manage domestic inflationary pressures, and thus maintain social stability. We consider that China has the ability to allow its currency to appreciate and put in place steps towards a free-floating framework, due to increased pricing power resulting from manufacturing of a wider range of value-added goods. Indeed, we have seen steps put in place to ready the country for appreciation of the currency, including conducting scenario analyses on local businesses, while concurrently increasing the internationalization of the currency. China is likely to become a global financial hub and a more attractive place for global business, as a bi-product of such initiatives. Such dynamics are likely to lead to ongoing strengthening in the Chinese currency over the foreseeable future.If I can find a summary, I'll post highlights of the Gloom Boom Doom market commentary, although in recent months it has been hard to find.

Friday, February 24, 2012

Jeremy Grantham's Quarterly Newsletter February 2012 Summary

Jeremy Grantham, GMO, has just released its Quarterly Newsletter entitled "The Longest Quarterly Letter Ever" a 15 pages report divided into 3 parts in contrast to his previous Letter "The Shortest Quarterly Letter Ever" with 4 pages only.

Part I: Investment Advice from Your Uncle Polonius

In the first part, which he could also have called "the 10 commandments of the individual investor", he gave 10 recommendations:

In the second section of the newsletter, Jeremy Grantham talks about the shortcomings of capitalism and how it focuses on short term gains and ignore long term pain. Examples are the current debt and resources depletion. The other problem is that capitalism buys (political) influence as was the case with tobacco companies that also insisted smoking tobacco was harmless, and now with energy companies that try to misinform the public and influence regulations.

The main problem, however, is capitalism inability to process finite resources and maintain rapid economic growth as it is mathematically impossible. Many people would cry foul if you say that a decline in population is necessary so that we can live peacefully. Some scientists also estimated that if Indian and Chinese were to catch the average American lifestyle, we would need 3 planets to live sustainably.

To conclude, he says that capital does thousands things better than other systems, but the 2 or 3 where it fails, could bring it down.

Part III: Investment Observations for the New Year

In the last part of the newsletter, he reflects on the year 2011 where most markets ended basically flat. Most equity markets are currently close to fair value, except the S&P 500 with expected returns of only 1% per year.

Overpricing exists in debt markets however. He sees great opportunities in avoiding duration in fixed income and recommend to underweight the most of the US market as a whole.

On the other end, natural gas is dirt cheap and the natural gas to crude oil ratio (BTU equivalent) is now 14% which is the lowest in 15 year. Anybody with a brain should look into investing in natural gas. Unfortunately, he did not give any specifics.

He also said that Gold producers look cheaper than Gold itself.

Finally, he gave GMO recommendations for the year ahead:

Part I: Investment Advice from Your Uncle Polonius

In the first part, which he could also have called "the 10 commandments of the individual investor", he gave 10 recommendations:

- Believe in history - Be patient and fair for assets to be at or below fair value

- Neither a lender nor a borrower be - Avoid leverage because it impacts an investor greatest asset: Patience

- Don't put all your treasure in one boat - If you diversify, your portfolio will be much more resilient

- Be patient and focus on the long term - Wait until markets are very cheap before making your move. Individual stocks usually recover, and markets always do.

- Recognize your advantages over the professional - Again, patience is your asset. Professional cannot wait to career and/or business risk (losing one's job or clients due to short term underperformance). You can afford to wait several years, professionals can't.

- Try to contain natural optimism - This is especially true for Australian and US investors that do not like to hear bad news

- But on rare occasions, try hard to be brave - You can't take bigger risks than professionals when markets are extremely mispriced even though it may come with pain in the short term.

- Resist the crowd: cherish numbers only - If you see your neighbors get rich during a bubble, do not jump on the wagon, follow some simple ratios that can help you estimate the markets over/udner valuation.

- In the end, it's quite simple. Really - Workout simple ratios and follow them. For example, the meaning reversion of profit margins and price earnings ratios. GMO does that for the 7-year market forecast.

- This above all: To thine own self be true - Know yourself. If you are easily influenced by others and cannot resist temptation during a bubble, you should NOT manage your own money.

In the second section of the newsletter, Jeremy Grantham talks about the shortcomings of capitalism and how it focuses on short term gains and ignore long term pain. Examples are the current debt and resources depletion. The other problem is that capitalism buys (political) influence as was the case with tobacco companies that also insisted smoking tobacco was harmless, and now with energy companies that try to misinform the public and influence regulations.

The main problem, however, is capitalism inability to process finite resources and maintain rapid economic growth as it is mathematically impossible. Many people would cry foul if you say that a decline in population is necessary so that we can live peacefully. Some scientists also estimated that if Indian and Chinese were to catch the average American lifestyle, we would need 3 planets to live sustainably.

To conclude, he says that capital does thousands things better than other systems, but the 2 or 3 where it fails, could bring it down.

Part III: Investment Observations for the New Year

In the last part of the newsletter, he reflects on the year 2011 where most markets ended basically flat. Most equity markets are currently close to fair value, except the S&P 500 with expected returns of only 1% per year.

Overpricing exists in debt markets however. He sees great opportunities in avoiding duration in fixed income and recommend to underweight the most of the US market as a whole.

- Inflation Hedges

- Resources

On the other end, natural gas is dirt cheap and the natural gas to crude oil ratio (BTU equivalent) is now 14% which is the lowest in 15 year. Anybody with a brain should look into investing in natural gas. Unfortunately, he did not give any specifics.

He also said that Gold producers look cheaper than Gold itself.

- European Complexity

Finally, he gave GMO recommendations for the year ahead:

- Heavily underweight U.S equities, but not the high quality quartile, which is almost fair price. Non-quality equities, in contrast, have a negative imputed 7-year return after their handsome rally in the last 3 months through to mid-February.

- Slightly overweight other global equities, which are almost fair price, down from a little cheap at year end.

- In total, be about neutral in global equities. Yes, there is more than our normal fair share of potential negatives lurking around, but on our data: a) most of the negatives are reflected in stock prices; and b) all fixed income duration is dangerously overpriced. This last situation is, of course, engineered by the Fed, which hopes to drive us all into taking more risk, notably by buying more equities. I hate to oblige, but at current equity prices it just makes sense to do what they want. As mentioned earlier, equities are also good long-term hedges against inflation.

- Underweight as much as you dare long-term bonds, especially higher-grade sovereign bonds.

- In the long term, resources in the ground, forestry, and agricultural land are attractive, but come with the usual caveats of the risk of short-term over pricing, so average in.

Tuesday, January 31, 2012

Marc Faber February 2012 Market Commentary

Marc Faber has just released his February 2012 market commentary on the gloomboomdoom.com website.

This month report is entitled "In all Investments it is a healthy Thing Now and Then to Hang a Question Mark on the Ideas we Have long Taken for Granted", implying that we should always reconsider the things we think of as obvious truth.

There is 1 attachment with this monthly market commentary (MMC) :

If I can find a summary, I'll post highlights of the Gloom Boom Doom market commentary a bit later.

This month report is entitled "In all Investments it is a healthy Thing Now and Then to Hang a Question Mark on the Ideas we Have long Taken for Granted", implying that we should always reconsider the things we think of as obvious truth.

There is 1 attachment with this monthly market commentary (MMC) :

- "2012: A Year of Reflation and Bursting of the "Bond Bubble"" by Michael A. Gayed,Chief Investment Strategist at Pension Partners, LLC

If I can find a summary, I'll post highlights of the Gloom Boom Doom market commentary a bit later.

Monday, October 31, 2011

Marc Faber November 2011 Market Commentary

Marc Faber has just released his November 2011 market commentary on his gloomboomdoom.com website.

This month report is entitled "The Strongest Principle of Economic Development Lies in Human Choices".

There are 2 attachments to the monthly market commentary (MMC) :

The second attachment refers to "Inflation, Deflation And The Fall Melt-Up of 2011" article on Seeking Alpha where Mr. Gayed explains how to navigate the markets which consistently changing market sentiments from deflation to inflation fear and vice-versa. He uses the price ratio of the Treasury Inflation Protected Bond ETF (TIP) relative to nominal 7-10 Year Treasuries (IEF) to anticipate sentiment.

I'll try to post highlights of the Gloom Boom Doom market commentary a bit later.

This month report is entitled "The Strongest Principle of Economic Development Lies in Human Choices".

There are 2 attachments to the monthly market commentary (MMC) :

- The Missing Chapter - A Personal View of Russia - Twenty Years After by Eric Kraus, Managing Director of Anyatta Capital

- The Inflation Pulse Returns and Implications on the Fall Melt-Up of 2011 by Michael A. Gayed, Chief Investment Strategist at Pension Partners, LLC

The second attachment refers to "Inflation, Deflation And The Fall Melt-Up of 2011" article on Seeking Alpha where Mr. Gayed explains how to navigate the markets which consistently changing market sentiments from deflation to inflation fear and vice-versa. He uses the price ratio of the Treasury Inflation Protected Bond ETF (TIP) relative to nominal 7-10 Year Treasuries (IEF) to anticipate sentiment.

I'll try to post highlights of the Gloom Boom Doom market commentary a bit later.

Sunday, October 30, 2011

Market Predictions for 2012 based on Trends

Last week, I reported Bloomberg Consensus of Predictions for Year-End 2012 in Where are Markets Headed for 2012 ?

That was their average forecast:

That was their average forecast:

- S&P 500: 1,428 vs Current: 1,229

- 10-year Treasury yield: 2.86% vs Current: 2.14%

- Inflation rate: 2.05% vs Current: 3.9%

- Unemployment rate: 8.7% vs Current: 9.1%

- GDP growth in fourth quarter: 2.5% vs Second quarter, 2011: 1.3%

- Gold price per ounce on Sept. 30, 2012: $1,835 vs Current: $1,704

- Value of euro: $1.40 vs Current: $1.39

- S&P/Case-Shiller 20-City Composite Home Price Index: 136.6 vs Current: 142.8

- Barrel of oil: $95 vs Current: $92.58

- S&P 500: 1000

- 10-Year Treasury yields: 2.5%

- Inflation Rate: 2.5%

- Unemployment Rate: 8.8%

- GDP Growth Rate: 1%

- Gold Price: 1850 USD

- Euro: 1.37 US dollar

- S&P Case-Shiller 20-City Composite Home Price Index: 135

- Barrel of Oil (WTI): 125 US dollar

Friday, October 28, 2011

Where are Markets Headed for 2012 ?

Bloomberg Consensus of Predictions for Year-End 2012 (unless otherwise noted):

1. UP Standard & Poor’s 500-stock index: 1,428 Current: 1,229

2. UP 10-year Treasury yield: 2.86% Current: 2.14%

3. DOWN Inflation rate: 2.05% Current: 3.9%

4. DOWN Unemployment rate: 8.7% Current: 9.1%

5. UP GDP growth in fourth quarter: 2.5% Second quarter, 2011: 1.3%

6. UP Gold price per ounce on Sept. 30, 2012: $1,835 Current: $1,704

7. UP Value of euro: $1.40 Current: $1.39

8. DOWN S&P/Case-Shiller 20-City Composite Home Price Index: 136.6 Current: 142.8

9. UP Barrel of oil: $95 Current: $92.58

Analysts are rather optimistic, except for the Case-Shiller index.

They also don't see huge swings in the markets (they never do).

Subscribe to:

Posts (Atom)